October 15, 2025

Stocks: Earnings, Economic Surprises, Policy Supportive Of Further Upside

October 2025

U.S. equities across the market capitalization spectrum produced gains in September with large caps leading the charge due to strength of the ‘Magnificent 7’ and beneficiaries of the mania surrounding artificial intelligence (AI) and the buildout of data centers. Breadth narrowed during the month, however, as communication services, consumer discretionary, information technology, and utilities led while cyclical areas more reliant on the path of the U.S. economy, such as energy, financials, and industrials lagged. Strong relative performance out of secular growth stocks tied to the AI theme is a reasonable base case in the coming months. Most active managers are trailing their benchmark and, as such, will buy any dip in these names or run the risk of chasing these stocks higher into the seasonally strong October through December stretch.

The consensus estimates for S&P 500 earnings in 2025 and 2026 were again revised higher, albeit modestly, in September, continuing a trend that has been in place since May. Positive earnings revisions have been supportive of improved investor sentiment in recent months, but weekly AAII surveys point to continued disbelief in the rally with those ‘bearish’ on U.S. stocks over the next six months still well above the historical average. This scenario provides a healthy backdrop for U.S. stocks to continue climbing a wall of worry. With the S&P 500 trading at almost 25 times projected 2025 earnings and 22 times expected 2026 earnings, trailing earnings likely matter little compared to the outlook/guidance provided. The bar perceived beneficiaries of AI and related spending must chin when providing commentary and forward guidance is now exceedingly high, with shortfalls likely punished severely.

While growth-oriented sectors powered gains in September, positive U.S. economic surprises stood out in the back-half of the month with durable goods orders surprising to the upside and jobless claims surprising to the downside, among other notable data points. This dynamic, should it persist, could lead to a broadening out of the rally with economically sensitive sectors participating in a more meaningful way if data continues to surprise to the upside. The Fed is increasingly focused on supporting the labor market after making a ‘risk management cut’ last month, and companies are seeking out ways to take advantage of the ability to immediately expense capital expenditures tied to the “One Big Beautiful Bill.” Thus, both monetary and fiscal policies appear supportive of further upside in U.S. stocks into 2026.

While we remain constructive on the outlook for U.S. stocks into year-end, we acknowledge that expectations and valuations for large caps provide little margin for error. However, old habits die hard, and investors will likely continue crowding into the largest, most well capitalized companies that make up a sizable slug of the S&P 500, thus limiting the depth of any near-term drawdown on guidance shortfalls.

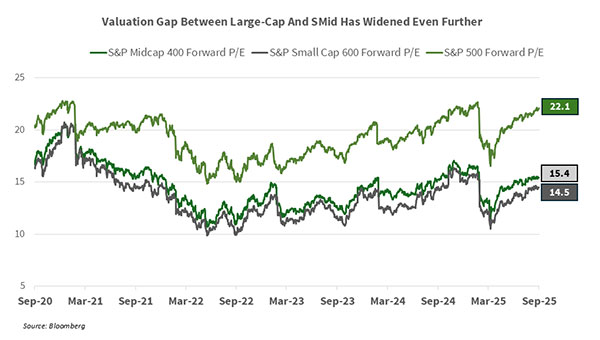

U.S. SMid A Potential Catch-Up Trade Into Year-End, And Beyond. The S&P Small Cap 600 and S&P Midcap 400 failed to build off momentum from August, producing only modest gains in September and lagging U.S. large and mega cap stocks in the process. After investors put the rate cut playbook into action after a lackluster July payrolls report, propelling the S&P 600 higher by 7% in August alone, they appeared to ‘sell the news’ and take profits in the wake of a 25-basis point rate cut at the FOMC’s mid-September meeting. This dynamic highlights to us that investors continue to view small and mid-cap stocks as little more than a trade and remain hesitant to reallocate capital that has been treated quite well in the S&P 500 into SMid over anything other than a short-term time horizon, but that’s where the opportunity lies.

This cohort of stocks remains under-owned and attractively valued with the S&P 400 trading at 15.4X projected 2026 earnings and the S&P 600 at 14.5X, compared to the S&P 500 at 22X projected 2026 earnings. Notably, even after 2Q25 earnings out of both the S&P 400 and S&P 600 easily topped consensus estimates, numbers for 3Q and 4Q have continued to trend lower. This backdrop provides a low bar for these companies in the coming quarters, and with U.S. economic data, on balance, surprising to the upside in the back-half of September, we view U.S. small, and particularly mid-caps as a potential catch-up trade into year-end and beyond.

Abroad, Tailwinds For Emerging, Headwinds For Developed Building. The MSCI Emerging Markets index gained 7% during September with exposure to China, Mexico, South Africa, South Korea, and Taiwan notable contributors as indices tied to each country rose 9% or more on the month. Momentum and broad-based strength behind the move higher in the MSCI EM index has been impressive and stands in contrast to the MSCI EAFE’s narrowing leadership profile. The MSCI EAFE developed markets index generated a 1.9% total return last month with country indices tied to Italy, Japan, and Spain all returning 1.5% or more on the month. On the other side of the ledger, Australia, Germany, and Switzerland, which together account for 25% of the MSCI EAFE index, closed out the month with modest losses of 1% or less.

Concerns surrounding potential political upheaval and a more uncertain outlook for fiscal policy are swirling across developed nations abroad, and investors are thus likely to be more cautious when allocating capital to developed markets abroad, a headwind for this cohort of stocks. Conversely, emerging markets, on balance, have the wind at their sails as capital expecting an improved growth outlook in the coming years has flowed into many of these economies, which has contributed to consistent strengthening of EM currencies since the end of April. With inflationary pressures easing and the U.S. dollar weaker versus a broad basket of EM currencies, central banks have more room to ease monetary policy to spur growth in the coming year, which should support a continued lift in stocks and bonds tied to developing markets.

As of October 9, 2025